Account B

Account B

January 1, 2024 actuarial valuation results

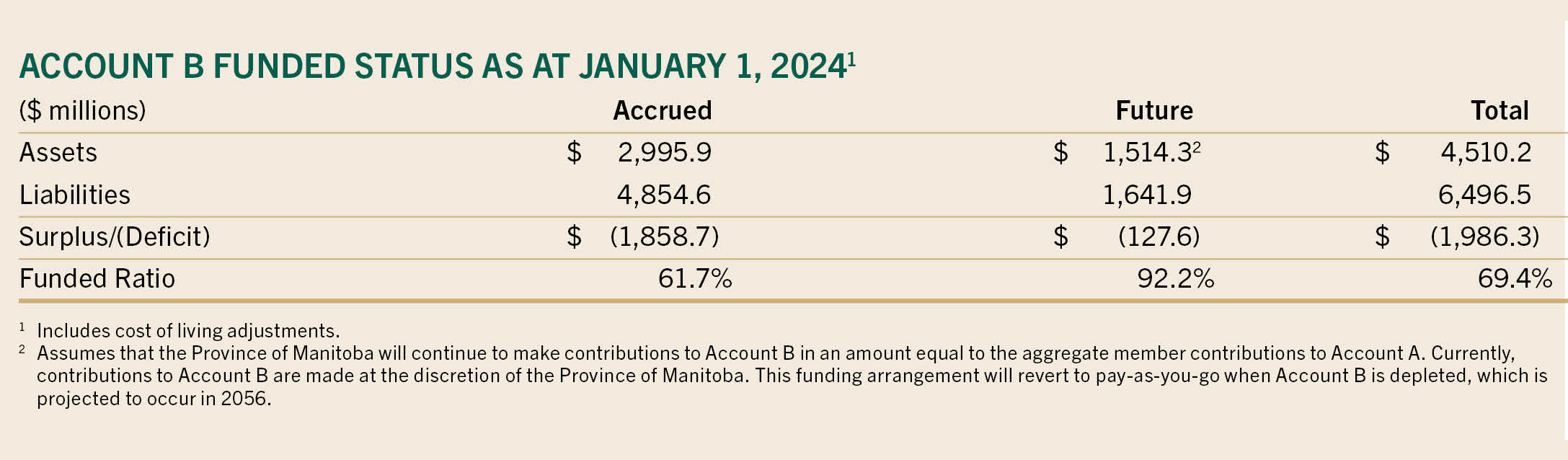

The most recent actuarial valuation of TRAF prepared by the plan actuary was as at January 1, 2024, which included an assessment of the financial condition of Account B. The valuation results for Account B are summarized in the following table.

The next actuarial valuation is scheduled to be performed as at January 1, 2027.

Actuarial valuations of the fund, including Account B, can be found in your Online Services account.

On a going-concern basis, as at January 1, 2024, Account B had an accrued deficit of $1,858.7 million (which is a deterioration from the $1,769.7 million accrued deficit at January 1, 2021). This equates to an accrued funded ratio of 61.7%.

Reconciliation to the prior valuation

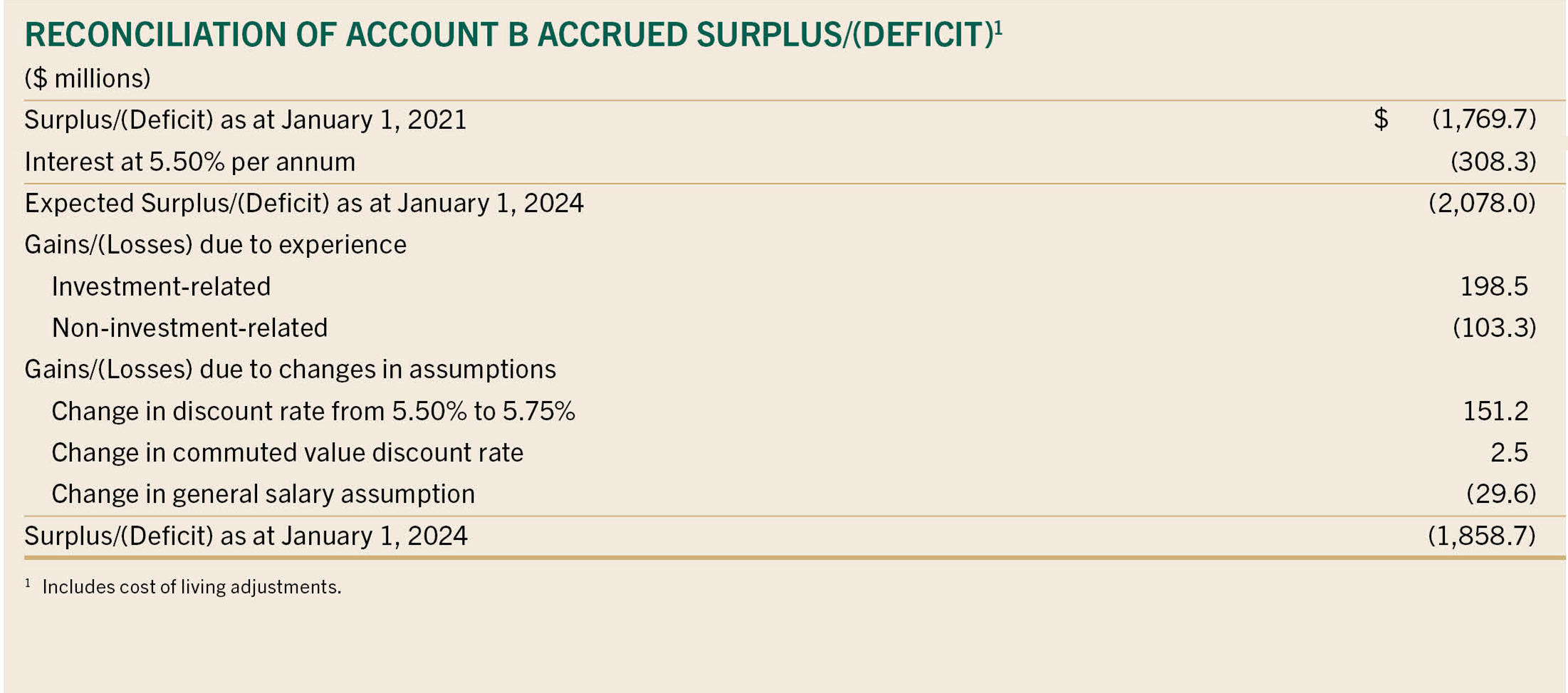

The table below reconciles the items that contributed to the Account B accrued deficit increasing from $1,769.7 million as at January 1, 2021, to a $1,858.7 million deficit as at January 1, 2024.

The primary factors with a positive impact on the funded status of Account B were the strong investment returns for the years 2021 to 2023 and the change in the discount rate assumption from 5.50% to 5.75%. The impacts were an improvement of $198.5 million and $151.2 million to the funded status, respectively. However, the interest on the deficit and non-investment related experience had negative impacts on the funded status. The impacts were decreases of $308.3 million and $103.3 million to the funded status, respectively.

January 1, 2025 extrapolated results

The accrued funded ratio of Account B was extrapolated to be 65.7% as at January 1, 2025. This figure was based on an extrapolation of the January 1, 2024, funded status. An extrapolation incorporates actual investment results, contributions received and benefits paid since the last formal valuation. The limitations are the plan’s actual experience with respect to mortality, retirement and termination since the date of the last valuation (i.e., the extrapolation will continue to rely on assumptions for these variables). The formal actuarial valuation as at January 1, 2024, revealed an accrued funded ratio of Account B of 61.7%. The funded ratio improvement was largely due to the net investment return being greater than the actuarial expected return during 2024.